General Insurance

Best Engagement Ring Insurance Options in 2026

Let me start with a quick story.

A friend of mine, let’s call her Sara got engaged on a random Tuesday evening. No fireworks. No viral proposal video. Just two people, takeout pizza, and a ring that honestly took her fiancé months of saving.

Fast forward three weeks later.

Sara goes to a café, washes her hands, and when she comes back… the ring is gone.

Cue panic. Cue tears. Cue the realization that love might be priceless, but engagement rings definitely are not.

That’s when the conversation around the best engagement ring insurance options in 2026 becomes very real and very necessary.

If you’re engaged (or about to be), this article is your “I wish someone told me sooner” moment.

Why Engagement Ring Insurance Is a Big Deal in 2026

Engagement rings today aren’t just jewelry. They’re:

- Emotional investments

- Financial commitments

- Often the most expensive personal item someone owns

In 2026, rings are getting more expensive, more customized, and more frequently worn. People wear their rings to the gym, while traveling, during daily errands, and even while working remotely at cafés.

That combo increases the risk of:

- Loss

- Theft

- Accidental damage

- Stones falling out

This is exactly why researching the best engagement ring insurance options in 2026 isn’t overthinking. It’s being smart.

What Engagement Ring Insurance Actually Covers

Before choosing a policy, it helps to know what good engagement ring insurance usually includes.

Most solid plans cover:

- Loss

- Theft

- Accidental damage

- Missing stones

- Mysterious disappearance

Many policies also include worldwide coverage, which matters more than ever in 2026.

What it typically does not cover:

- Normal wear and tear

- Intentional damage

- Neglect or poor maintenance

Understanding this difference helps you pick the best option, not just the cheapest one.

How Engagement Ring Insurance Works (Without the Boring Stuff)

Think of engagement ring insurance like this:

- Your ring is insured based on its appraised value

- You pay a small monthly or annual premium

- If something happens, you file a claim

- You receive a repair, replacement, or payout depending on your policy

It’s simple, practical, and designed to reduce stress.

Best Engagement Ring Insurance Options in 2026 (Honest Breakdown)

Now let’s get into the real comparisons. These are widely considered the best engagement ring insurance options in 2026, based on coverage quality, flexibility, and ease of use.

1. Jewelers Mutual

Jewelers Mutual remains one of the most trusted names in engagement ring insurance.

Why it stands out in 2026:

- Coverage for loss, theft, and damage

- Optional zero-deductible plans

- Freedom to choose your own jeweler

- Worldwide protection

Best for:

People who want comprehensive coverage and long-term reliability.

2. BriteCo

BriteCo is popular with modern couples and owners of high-value or lab-grown diamonds.

Why people choose it:

- Fast, digital setup

- Competitive premiums

- Replacement rings match original quality, not downgraded versions

Best for:

Tech-savvy buyers and anyone who values speed and transparency.

3. Lemonade Jewelry Insurance

Lemonade has become a go-to option for younger couples and first-time ring owners.

Why it works:

- Affordable monthly pricing

- Easy app-based claims

- Clear, straightforward policies

Things to consider:

Coverage limits may be lower for very high-value rings.

Best for:

Budget-conscious couples who want simple protection without complexity.

4. Homeowners or Renters Insurance Riders

Some people add their engagement ring to an existing home or renters policy.

Pros:

- Convenience

- One combined insurance bill

Cons:

- Claims can increase home insurance premiums

- Higher deductibles

- Limited coverage compared to standalone policies

In 2026, most experts still recommend standalone engagement ring insurance for better protection.

5. Boutique or Jeweler-Based Insurance

Some jewelers now offer in-house insurance options.

Why they’re trending:

- Personalized coverage

- Often tied directly to repair or replacement services

Important tip:

Always confirm coverage applies beyond that single store and includes loss, not just damage.

A Small Story That Makes It Real

Back to Sara.

She did not have engagement ring insurance when her ring disappeared.

The café checked cameras. Nothing turned up. Lost and found was empty.

Eventually, she replaced the ring herself.

This time, though, she insured it.

Now she wears her ring daily without stress. Travel, workouts, life, no constant fear of “what if.”

That peace of mind alone made the insurance worth it.

How Much Does Engagement Ring Insurance Cost in 2026?

Here’s the part most people are surprised by.

Engagement ring insurance usually costs about:

- 1% to 2% of the ring’s value per year

For example:

- A $5,000 ring typically costs $50–$100 annually to insure

That’s often less than phone insurance, yet it protects something far more meaningful.

How to Choose the Best Engagement Ring Insurance Option for You

Ask yourself a few simple questions:

- Do I wear my ring every day?

- Do I travel often?

- Is my ring custom or high-value?

- Do I want cash replacement or same-quality replacement?

If maximum protection matters most, standalone insurers like Jewelers Mutual or BriteCo are usually the best choice.

If affordability is the priority, Lemonade can be a strong option.

Common Engagement Ring Insurance Myths

“I’ll never lose my ring.”

Most people who lose a ring believe the same thing.

“Insurance is too expensive.”

It’s usually very affordable compared to the ring’s value.

“I’m careful, so I don’t need it.”

Accidents don’t care how careful you are.

In 2026, engagement ring insurance is less about fear and more about smart planning.

Final Thoughts

The best engagement ring insurance options in 2026 are not about being overly cautious.

They’re about freedom.

Freedom to wear your ring confidently.

Freedom to live your life normally.

Freedom from stress if something unexpected happens.

If your engagement ring represents love, effort, and a serious financial investment, protecting it just makes sense.

Imagine a world where surviving longer doesn’t just mean more birthdays, it literally pays you.

Sounds like sci-fi, right? But for a growing number of billionaires, living to 120 isn’t just a dream, it’s a calculated investment, a lifestyle, and in some cases, a financial strategy. From cutting-edge biotech to unusual insurance products, the ultra-wealthy are quietly turning longevity into a high-stakes game where the ultimate jackpot is time itself.

Let’s break down this wild concept: the idea that staying alive longer than almost anyone else could actually make you money.

The New Obsession: Outliving Death

Humans have always been obsessed with living longer. From ancient myths to modern medicine, the idea of beating death has never gone out of style. But today, that obsession has evolved into something much bigger and much more expensive.

The modern longevity industry is exploding, with billions pouring into research aimed at slowing or even reversing aging. In fact, this sector is now worth tens of billions globally and growing fast.

At the center of it all? Billionaires.

Tech elites and ultra-wealthy investors are pouring money into startups, research labs, and experimental therapies. Their goal isn’t just to live longer it’s to push the boundaries of human lifespan, possibly beyond 120 years.

And unlike the average person, they have the resources to treat aging like a problem that can be solved.

Meet the “Live to 120” Club

Some of the world’s richest individuals are openly chasing extreme longevity.

- Tech investor Peter Thiel has long been fascinated with defeating aging.

- Oracle founder Larry Ellison invests heavily in anti-aging research.

- Biohacker Bryan Johnson follows a strict daily routine designed to reverse his biological age.

These aren’t just casual health goals. These individuals are investing millions into personalized regimens, strict diets, advanced medical treatments, and experimental science all in pursuit of extending life.

Some even believe that if they can just make it to around 120 years old, future science might allow them to live indefinitely.

Yeah… basically, “live long enough to live forever.”

The Twist: Getting Paid to Live Longer

Here’s where things get really interesting.

There’s a concept in finance called longevity insurance and it flips traditional insurance on its head.

Normally, life insurance pays out when you die. But longevity-based financial products reward you for doing the opposite: staying alive longer than expected.

According to financial experts, longevity insurance works like a “reverse life insurance.” Instead of paying your family after death, it provides income if you live far beyond average life expectancy.

Think of it like this:

- You invest early.

- You survive longer than most people.

- You start receiving payouts later in life (like at 85, 90… or beyond).

In simple terms: you win by not dying.

Why This Exists: The Longevity Risk Problem

This might sound cool, but it actually comes from a real financial problem: longevity risk.

Longevity risk is the danger that people live longer than expected and run out of money. Governments, pension systems, and insurance companies are all struggling with this.

Because if people start living to 100… or 120… retirement systems break.

That’s why new financial products are emerging to handle this reality. And for the wealthy, these tools aren’t just protection, they’re strategy.

Billionaires Treat Longevity Like an Investment Portfolio

Here’s the mindset shift: billionaires don’t see health as just “wellness.”

They see it as ROI (return on investment).

Instead of spending money to treat illness, they spend aggressively to prevent aging itself.

Typical strategies include:

- Personalized medical teams

- Advanced diagnostics and full-body scans

- Stem cell therapies and experimental drugs

- Strict nutrition and fitness protocols

- Continuous health tracking

These aren’t casual habits. They’re optimized systems designed to extend both lifespan and “healthspan” (how long you stay healthy).

Some even follow extreme routines fasting for hours daily, tracking every calorie, and optimizing sleep like it’s a business metric.

The Business of Living Longer

The crazy part? This isn’t just personal, it’s a massive industry.

The anti-aging and longevity market is expected to reach hundreds of billions of dollars globally.

Why?

Because aging is the ultimate universal problem.

Everyone wants more time but only a few can currently afford the most advanced solutions.

This creates a huge gap:

- The wealthy invest in cutting-edge life extension.

- The average person gets traditional healthcare.

And that gap could widen dramatically if breakthroughs actually work.

The Dark Side: Is This Just a Rich People Game?

Not everyone is hyped about this.

Critics argue that the obsession with living longer is less about improving life and more about avoiding death at all costs.

Some believe it’s driven by fear rather than purpose.

And there’s a real ethical question:

What happens if only the rich can afford to live significantly longer?

Imagine a world where billionaires routinely live to 120 while everyone else doesn’t.

That’s not just a health issue, it’s a societal shift.

The Reality Check: Can Humans Actually Reach 120?

Right now, the longest confirmed human lifespan is 122 years.

So technically, it’s possible but extremely rare.

Science is making progress, but there’s still no guaranteed way to consistently reach 120, let alone go beyond it.

Many experts say we can extend healthy years but “immortality” is still far away.

Even among billionaires, results are uncertain.

The Future: A World Where Living Longer Pays

Despite the uncertainty, one thing is clear:

Longevity is becoming financialized.

In the future, we might see:

- More “live longer, earn more” insurance products

- Investments tied to health outcomes

- Personalized longevity plans like retirement portfolios

- Entire economies built around extending human life

For billionaires, this is already happening.

They’re not just trying to live longer they’re betting on it.

Final Thoughts: The Ultimate Flex?

So yeah… getting paid to stay alive sounds wild but it’s real.

For the ultra-wealthy, longevity is no longer just about health. It’s a mix of science, finance, and ambition.

They’re essentially asking:

What if death… was optional (or at least delayed)?

And more importantly:

What if surviving longer made you richer?

For now, it’s a game only a few can play.

But if science keeps evolving, this “billionaire bet” might one day become everyone’s reality.

Until then… staying alive is still free but maybe not for long.

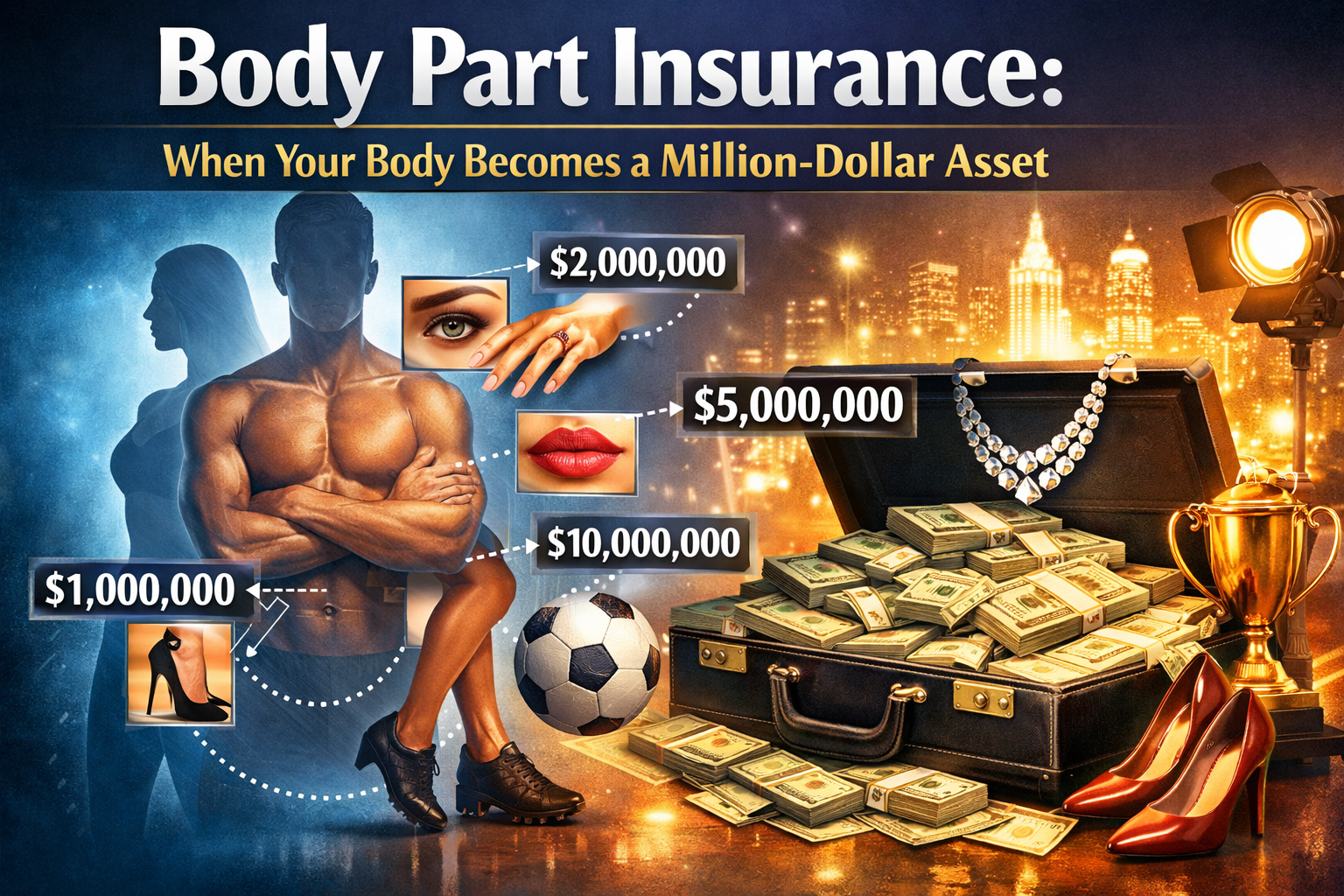

What if your lips were worth millions… or your hair… or even your taste buds? Sounds unreal, but in today’s world of celebrity branding and high-stakes careers, body part insurance is very real and getting bigger.

From Hollywood icons to athletes and even niche professionals, people are turning their physical features into protected financial assets. And the numbers? Absolutely insane.

What Is Body Part Insurance (Deeper Look)?

Body part insurance isn’t a standard policy you can just click and buy online. It usually falls under specialty insurance (often through companies like Lloyd’s of London).

Here’s how it works:

- A person identifies a body part critical to their income

- Insurers assess its value (based on earnings, brand deals, future potential)

- A policy is created to cover damage, loss, or reduced function

- If something happens → payout kicks in

It’s basically treating your body like a business asset.

How Do They Decide the Value?

This part is actually super interesting.

Insurance companies don’t just guess a number they calculate:

- Current income tied to that body part

- Future earning potential

- Market demand (how unique or recognizable it is)

- Risk level (injury chances, lifestyle, profession)

That’s how we end up with numbers like $300 million for legs 😳

More Crazy Real-Life Stories (Gets Wilder 👇)

⚽ David Beckham – The $195 Million Whole Body

David Beckham reportedly insured his entire body for around $195 MILLION.

Why? Because he wasn’t just a footballer he was a global brand. His looks, physique, and presence brought in massive endorsement deals.

🎸 Keith Richards – The $1.6 Million Hands

The legendary guitarist insured his hands for about $1.6 MILLION.

Without them? No guitar. No performances. No income. Simple.

🦵 Heidi Klum – Uneven Legs Worth Millions

Heidi Klum insured her legs—but here’s the twist:

- One leg was valued higher than the other 😭

Total value? Around $2 MILLION

Yes, even tiny differences matter at that level.

🍗 Betty Grable – The Original Million-Dollar Legs

Back in the 1940s, Betty Grable insured her legs for $1 MILLION—which today would be worth over $20+ MILLION adjusted for inflation.

She basically started the trend.

👃 Troy Polamalu – The $1 Million Hair

This one’s iconic.

Troy Polamalu insured his hair for $1 MILLION because it was part of his identity—and even featured in commercials.

👅 Rihanna – The $1 Million Legs

Rihanna reportedly insured her legs for $1 MILLION after winning a “best legs” award.

Brand deals + beauty recognition = $$$

The Weirdest Body Parts Ever Insured 🤯

This is where it gets kinda crazy:

- Taste buds → insured by professional food tasters

- Noses → perfume experts rely on them

- Beards → some celebrities have insured facial hair

- Chest hair → yes, even that has been insured 💀

- Butts → rumored in entertainment industry

Basically, if it can make money… it can be insured.

Can Normal People Do This?

Short answer: yes—but with limits

You don’t need to be a celebrity, but you do need:

- Proof that your income depends on that body part

- A high enough earning level

- A legit reason for risk coverage

Examples:

- A surgeon insuring their hands

- A dancer insuring their feet

- A YouTuber/influencer insuring their appearance

It’s rare but not impossible.

The Hidden Risks (Not All Glamorous)

This isn’t just flexing money—there are downsides too:

1. Expensive Premiums

You might pay thousands (or millions) yearly just to keep the policy active.

2. Strict Conditions

Some policies limit activities:

- No extreme sports

- No risky behavior

- Lifestyle monitoring 👀

3. Claim Challenges

Insurance companies investigate claims deeply. You can’t just say “my voice is off today” and expect millions.

The Business Side of It

This whole industry is growing because of:

- Influencer economy

- Personal branding

- Social media fame

- High-value endorsements

Today, a face or voice can be worth more than a traditional job.

So people are thinking:

“If I insure my car… why not my face?”

Future of Body Part Insurance

This is where things get even more interesting.

In the future, we might see:

- Influencers insuring their Instagram face

- Gamers insuring their hands & reaction time

- AI creators insuring their voice clones

- Virtual influencers insuring digital identity

Yeah… it’s going to get even crazier.

Final Thoughts

Body part insurance might sound like a flex, but it’s actually:

👉 Smart risk management

👉 Brand protection

👉 Financial securityIn a world where you are the product, protecting your most valuable asset just makes sense.

Breakups are messy. Emotionally, socially… and surprisingly, financially.

Now imagine this: your relationship ends, and instead of just dealing with heartbreak, you get money back.

Sounds like something out of a satire blog, but breakup insurance is a real (and growing) niche. It sits at the intersection of modern dating, financial planning, and a slightly cynical view of love.

Let’s get into it.

What Is Breakup Insurance, Really?

Breakup insurance isn’t about putting a price on your feelings. No company is handing out checks because someone left you on read for three days.

Instead, it focuses on financial damage caused by relationships ending.

Think about all the money tied into modern relationships:

- Flights booked months in advance

- Non-refundable hotel reservations

- Wedding venues and deposits

- Shared leases or furniture

Breakup insurance steps in to cover those losses when things fall apart.

So it’s less “get paid for heartbreak” and more:

“at least I’m not broke and heartbroken.”

Where It Actually Exists (And Works)

The most practical and widely used form of breakup insurance is tied to travel.

Some booking platforms and insurance add-ons allow you to cancel a trip if your relationship ends before departure. Instead of losing everything, you get a partial refund.

Real Scenario

A couple in the UK booked a luxury vacation to Santorini—flights, hotel, activities, the full romantic package. A few weeks before departure, they broke up.

Normally, that’s a total loss. Thousands gone.

But because they had a breakup-related cancellation policy, one of them was able to cancel and recover most of the cost. No awkward solo honeymoon, no begging customer support for exceptions.

It turned a financial disaster into a manageable inconvenience.

Wedding Insurance: Where Things Get Serious

If travel insurance is the casual version, wedding insurance is where things become high-stakes.

Weddings are expensive. Like, painfully expensive.

And they’re planned months, sometimes years in advance.

Real Story

In the U.S., a couple had spent over $30,000 on their wedding. Two months before the date, the engagement fell apart.

Without insurance, that money would have been mostly gone venue deposits, catering, decorations, everything locked in.

But because they had wedding insurance that included cancellation coverage, they were able to recover a large portion of the costs.

Still a breakup. Still painful. But not financially devastating.

The Wild Side: Betting on Love

Not all breakup insurance is practical or even legal.

In China, there was a bizarre trend where people could essentially “insure” celebrity relationships.

Here’s how it worked:

- You pay a small amount of money

- Choose a celebrity couple

- If they break up within a certain time, you get paid

It turned relationships into a betting market. Fans weren’t just emotionally invested—they were financially invested.

As you can imagine, regulators shut it down pretty quickly. It blurred the line between insurance and gambling, and raised some serious ethical questions.

Still, it showed something interesting:

People are willing to treat relationships like probabilities.

Everyday “Unofficial” Breakup Insurance

Even without formal policies, people create their own versions of breakup insurance.

Real-Life Examples

- Someone keeps a separate savings account “just in case” a relationship ends

- Couples split big purchases carefully instead of merging finances

- One partner keeps their old apartment lease active during the early stages of moving in

It’s not romantic, but it’s practical.

One Reddit user put it bluntly:

“I loved him, but I also loved having a backup plan.”

Why This Trend Is Growing

Breakup insurance didn’t just appear randomly. It reflects how relationships have changed.

Modern dating is faster, more expensive, and more intertwined with lifestyle.

People:

- Travel together early in relationships

- Move in faster than before

- Spend heavily on shared experiences

- Plan big events like weddings earlier

At the same time, breakups are still common.

That combination of high emotional risk plus high financial investment creates demand for protection.

It’s not about expecting failure. It’s about acknowledging reality.

The Awkward Question: Does This Kill the Romance?

There’s definitely a weird vibe to ensuring your relationship.

Some people see it as smart and responsible.

Others see it as a red flag.

Because let’s be honest bringing up breakup insurance in a relationship conversation sounds like:

“I trust you… but also I’ve read the statistics.”

That tension is what makes this topic so interesting. It sits right between logic and emotion.

The Limits of Breakup Insurance

Here’s where things get complicated.

Insurance works best when risks are:

- Random

- Measurable

- Hard to manipulate

Breakups don’t fit neatly into that.

What counts as a breakup?

What if a couple pretends to split just to claim money?

How do you verify emotional events?

Because of this, most companies avoid offering direct “breakup payouts.”

They stick to covering objective, verifiable losses like cancelled bookings or contracts.

Where This Could Be Heading

Breakup insurance is part of a larger shift toward hyper-personalized insurance.

We already insure things that would have sounded strange a decade ago:

- Pets

- Digital content

- Events

- Even parts of a person’s body in some industries

So it’s not unrealistic to imagine more relationship-related coverage in the future.

Maybe not “heartbreak insurance,” but definitely more policies tied to life events triggered by relationships.

Final Thought

Breakup insurance sounds like a joke at first.

But the more you look at it, the more it makes sense.

It doesn’t mean people believe their relationships will fail.

It just means they’ve seen enough of life to know that sometimes… things don’t go as planned.

And if you can’t protect your heart, at least you can protect your wallet.

Get Paid to Stay Alive? The Billionaire Bet on Living to 120

Body Part Insurance: When Your Body Becomes a Million-Dollar Asset

Get Paid to Break Up? Inside the World of Breakup Insurance

How Much Is Health Insurance a Month?

Will Insurance Cover Ozempic? This Information Tells You the Truth

What Does Life Insurance Cover?7 Must-Known Facts to Protect Your Loved Ones!

-

Health Insurance1 year ago

How Much Is Health Insurance a Month?

-

General Insurance1 year ago

Will Insurance Cover Ozempic? This Information Tells You the Truth

-

Life Insurance1 year ago

Life Insurance1 year agoWhat Does Life Insurance Cover?7 Must-Known Facts to Protect Your Loved Ones!

-

Auto Insurance1 year ago

Auto Insurance1 year agoWhy Is My Auto Insurance So High? There Is a Secret Behind High Auto Insurance Costs That Goes Unknown

-

General Insurance4 months ago

Can Cowboys Get Life Insurance?

-

Life Insurance1 year ago

Life Insurance1 year agoWhat Is Life Insurance? Everything You Need to Know!

-

Health Insurance3 months ago

Health Insurance3 months agoMobility Scooter Insurance: What It Is, Why You Need It, and How to Choose the Best Policy

-

Health Insurance3 months ago

Health Insurance3 months agoPrima Car Insurance Reviews: Is It the Right Choice for Your Ride?