General Insurance

Is Business Insurance Required by Law?

Business insurance is necessary and is not optional as many people believe. In the majority of instances it is mandated by law such as workers compensation or commercial auto insurance. Although not mandatory, insurance ensures that your business is not affected by legal and financial risks.

What Are the Legally Mandated Business Insurance

As we have now cleared up the confusion surrounding the issue of whether business insurance is mandatory or not, we will now move on to explain what exactly you need to have. Being aware of the required coverage according to the law can get you out of major financial problems in the future.

1. Workers Compensation Insurance.

This is mandatory by law in most states where you have employees. It reimburses medical expenses and lost earnings in case one is injured in the workplace. Failure to do it might result in huge fines.

2. General Liability Insurance.

Not obligatory, but nearly always obligatory. It insures you against claims such as damage of property or injuries and most clients or landlords will not do business with you without this.

3. Commercial Auto Insurance

This is a required coverage in case your business operates on vehicles. Personal car insurance will not defend you when you use the car on business and therefore make sure that your cars are insured.

4. Professional Liability Insurance.

Necessary in numerous careers such as law, medicine or consulting. It helps you to avoid client lawsuits on account of error or oversight – needed by service-related companies.

5. Other Required Coverage’s

In certain states or industries, unemployment, disability or special insurance is also required. Business insurance laws should be checked in any state to make sure that the laws are being abided by.

Should Small Businesses and Startups Buy Business Insurance?

A lot of small business owners believe that only a large business needs insurance but that is not the case. Small business, startup companies, and home based companies also need business insurance just as much.

Although it may not be a mandatory thing as required by law, it can help you avoid huge financial losses. One accident, suitcase or even destruction of property would simple cost more than you earn in a year.

Unless you do not have employees, workers should be insured by workers compensation in most states. Commercial auto insurance is a necessity in case you use vehicles. And in case you rent an office, landlords tend to demand general liability.

In the case of home-based businesses, home insurance will not address business related problems hence smart to get individual coverage. Also, most of your clients will not do business with you unless you can supply evidence of insurance – this creates confidence and professionalism.

To summarize, though business insurance may not be mandatory in law, it is one of the best decisions you can make in order to save your small business and its future.

Should LLCs and Self-Employed persons have Business Insurance?

Most individuals assume that when they form an LLC, all the risks are automatically covered to them, which is not the case. LLP securing your business is not securing your personal assets. That is where business insurance is applied.

Therefore, does LLC require business insurance?

Not necessarily – again not in every instance, but in most instances it is legally stipulated or contractually obligatory. For example:

· Your LLC may need workers compensation insurance which is normally mandated by law in case your LLC has employees.

· In case you are using company cars, commercial automobiles insurance is obligatory.

· In the case of professional services providers, professional liability insurance can be a mandatory requirement by customers or licensing authorities.

Although this may not be compulsory, the experts suggest that every LLC has a general liability insurance to cover accidents, property damages, or claims of injuries.

Are self-employed people now required to have business insurance?

Yes — and it’s a smart move. Freelance and one-person businesses are not that safe. Only one mistake, conflict with the client or broken windows may result in expensive litigation. Professional liability insurance (errors and omissions insurance) is useful in times when something may go wrong.

Moreover, a lot of clients want to cooperate with insured specialists – they demonstrate confidence and credibility. Even sole proprietors are at risk of losing either personal savings or assets in the event of a lawsuit without coverage.

In short:

Regardless of whether you are operating a freelance business, LLC or a small startup, business insurance helps in covering your work, income and future. Neither is it merely legal formalities, it is peace of mind.

What Would Be the Alternative to Not Having Business Insurance?

It is common to find that many business owners risk opting out of insurance because of financial reasons, yet this would cost them a lot in the end. Risk of loss of money, law suits and even closing of your business are all there to you working without business insurance.

The following is what may occur in the absence of business insurance:

· You will be out of pocket when it comes to damages or lawsuits.

You will have to pay all expenses on your own in case a customer suffers injuries, your gadget malfunctions, or you are sued. Only one such allegation can drain your bank account or put you out of business.

· The consequences might include legal fines.

Certain coverage’s, such as workers’ compensation or business auto insurance are mandatory. In some states they can result in fines, suspension of the license and even criminal charges should they not be had.

· You may lose clients or contracts.

Before associating with many clients, landlords, and partners request evidence of insurance. It is something that you might be losing deals or may have a hard time growing your business without.

· Your reputation would be hurt.

Uninsured is not a good idea to project your business as unprofessional or unreliable, particularly when your competitors are adequately insured.

In short:

You may save money by not taking up business insurance at present; but you may ruin your business in the future. It is much more intelligent and safe to insure all you have built.

Optimal Time of the Year to Buy Business Insurance

The question many new business owners would ask is –when to buy business insurance? The ideal response is prior to commencing business.

The most opportune moment to get business insurance is as you establish your business at hand, before you enter into a contract, employing workers or just starting to work with customers. This is because risks begin when you get in business. A single accident, a spoiled good or a customer complaint prior to your insurance may cause huge losses.

Here’s a quick guide:

· Starting a new business? Get coverage prior to your launch date.

· Hiring employees? Employees will probably require workers compensation insurance immediately (in most states it is legally mandatory).

· Signing a lease or contract? The majority of the landlords and clients will request you to provide them with evidence of general liability insurance before they can transact business with you.

· My services to be expanded or altered? Add or renew a new coverage according to your growth.

In a nutshell:

The sooner the better. The advantages of buying business insurance before your first project or sale are that you will be covered since day one- and you will not likely end up in financial and legal snarls in the future.

Casinos com Multibanco em Portugal – Guia Prático para Jogadores

1. O que são os casinos com Multibanco?

Em Portugal, casinos com Multibanco em Portugal referem‑se a plataformas de jogo online que permitem depositar e levantar fundos diretamente através da rede de caixas automáticas Multibanco. Esta forma de pagamento é a mais usada pelos portugueses porque é rápida, segura e não exige cartão de crédito.

Ao escolher um casino que aceita Multibanco, o jogador tem acesso a um método de pagamento familiar, com possibilidade de usar o número de referência gerado na hora. O valor aparece na conta em minutos, o que facilita o controlo do dinheiro disponível para apostar.

2. Como criar a tua conta e passar pela verificação

O processo de registo costuma ser simples: basta preencher nome, data de nascimento, endereço de e‑mail e criar uma senha. Depois, o casino enviará um código de verificação por e‑mail ou SMS para confirmar a identidade.

Para concluir a KYC (Know Your Customer) e poder fazer levantamentos, vais precisar de:

- Cópia do Cartão de Cidadão ou Passaporte

- Comprovativo de morada (fatura de água, luz, etc.)

- Extrato bancário que mostre o teu nome completo

Alguns casinos aceleram a verificação se o utilizador confia num serviço de verificação automática, mas a maioria ainda pede o envio manual de documentos. O prazo normal varia entre 24 e 48 horas.

3. Bónus de boas‑vindas e condições de aposta

Um dos motivos de atrair jogadores são os bónus de boas‑vindas. Normalmente, esses bónus chegam em duas formas: match bonus (por exemplo, 100 % até 200 €) e rodadas grátis nos slots mais populares.

É crucial olhar para os wagering requirements. Um bónus com 30x o valor depositado significa que terás de apostar 30 vezes esse montante antes de poder retirar os ganhos. Casinos mais transparentes anunciam claramente o RTP médio dos jogos aos quais o bónus se aplica.

Exemplo de cálculo de requisito de aposta

Se depositares 100 € e receberes um bónus de 100 €, o total a apostar será 200 € × 30 = 6 000 €. Só então poderás fazer um levantamento sem penalizações.

4. Métodos de pagamento e velocidade de levantamento

Além do Multibanco, a maioria dos sites aceita cartões Visa/Mastercard, Paysafecard e sistemas de carteiras eletrónicas. No entanto, o Multibanco continua a ser o método preferido para depósitos porque permite controlar exatamente quanto se entra na conta do casino.

Quanto à velocidade de levantamento, os casinos que utilizam Multibanco costumam processar o pedido em até 24 horas úteis, mas alguns oferecem instant payouts quando o método escolhido é carteiras eletrónicas ou transferências bancárias internas.

5. Experiência mobile e aplicativos dedicados

Jogadores que preferem usar o telemóvel podem descargar a aplicação oficial do casino ou aceder ao site via navegador. As apps nativas geralmente têm melhor performance, notificações de bónus em tempo real e suporte a pagamentos Multibanco através de QR‑code.

Se preferires jogar em navegador, verifica se o site oferece um layout responsivo e se todas as funcionalidades (como live casino e sportsbook) funcionam sem atrasos. As versões mobile tendem a ser mais leves, o que importa se a ligação à internet não for muito rápida.

6. Segurança, licenciamento e jogo responsável

Todos os casinos com Multibanco em Portugal legalmente operam sob licença da Entidade Reguladora do Jogo (ERG). Essa licença garante que os jogos são auditados por entidades independentes, proporcionando um RTP justo e evitando práticas desleais.

Além da licença, procura indicadores de segurança como o selo SSL e a disponibilidade de ferramentas de responsible gambling: limites de depósito, auto‑exclusão e suporte especializado em caso de necessidade.

7. Comparativo rápido dos principais casinos (tabela)

| Casino | Bónus de Boas‑Vindas | RTP Médio | Velocidade de Levantamento | Licença ERG |

|---|---|---|---|---|

| Casino A | 100 % até 300 € + 50 rodadas | 96,5 % | Até 24 h (Multibanco) | Sim |

| Casino B | 200 % até 200 € | 95,8 % | Instantâneo (eWallet) | Sim |

| Casino C | 150 % até 250 € + 30 rodadas | 97,2 % | 48 h (Bank Transfer) | Sim |

Esta tabela ilustra como os fatores variam entre plataformas. Analisa qual combinação de bónus, RTP e velocidade de levantamento se alinha mais com o teu estilo de jogo.

8. Dicas finais para escolher o melhor casino Multibanco

Para tomar a decisão certa, segue estas recomendações práticas:

- Confirma que o casino possui licença ERG e usa encriptação SSL.

- Compara os requisitos de aposta dos bónus – quanto menor, melhor.

- Verifica a rapidez dos levantamentos via Multibanco e se há limites mínimos.

- Experimenta a versão mobile antes de te comprometeres financeiramente.

- Utiliza as ferramentas de jogo responsável para definir limites claros.

Se ainda estiveres em dúvida, consulta a lista dos melhores casinos online Multibanco para portugueses e escolhe a que melhor corresponde às tuas necessidades.

9. Perguntas frequentes (FAQ)

Posso usar o Multibanco para levantar fundos?

Sim, a maioria dos casinos oferece a opção de retirada via Multibanco, geralmente com um custo reduzido e tempo de processamento de até 24 horas.

O que acontece se eu não cumprir os requisitos de aposta?

Se não completes o wagering requirement, o bónus e os ganhos associados podem ser expirados, e o casino pode cancelar o teu saldo relacionado ao bónus.

Os casinos online são seguros?

Os que operam com licença ERG devem obedecer a padrões rigorosos de segurança, auditoria de software e proteções de dados. Sempre verifica o selo SSL e lê as políticas de privacidade.

Existe apoio ao cliente em português?

Os principais casinos têm suporte em português via chat ao vivo, e‑mail e telefone. A disponibilidade 24/7 é um bom indicador de atenção ao cliente.

Imagine a world where surviving longer doesn’t just mean more birthdays, it literally pays you.

Sounds like sci-fi, right? But for a growing number of billionaires, living to 120 isn’t just a dream, it’s a calculated investment, a lifestyle, and in some cases, a financial strategy. From cutting-edge biotech to unusual insurance products, the ultra-wealthy are quietly turning longevity into a high-stakes game where the ultimate jackpot is time itself.

Let’s break down this wild concept: the idea that staying alive longer than almost anyone else could actually make you money.

The New Obsession: Outliving Death

Humans have always been obsessed with living longer. From ancient myths to modern medicine, the idea of beating death has never gone out of style. But today, that obsession has evolved into something much bigger and much more expensive.

The modern longevity industry is exploding, with billions pouring into research aimed at slowing or even reversing aging. In fact, this sector is now worth tens of billions globally and growing fast.

At the center of it all? Billionaires.

Tech elites and ultra-wealthy investors are pouring money into startups, research labs, and experimental therapies. Their goal isn’t just to live longer it’s to push the boundaries of human lifespan, possibly beyond 120 years.

And unlike the average person, they have the resources to treat aging like a problem that can be solved.

Meet the “Live to 120” Club

Some of the world’s richest individuals are openly chasing extreme longevity.

- Tech investor Peter Thiel has long been fascinated with defeating aging.

- Oracle founder Larry Ellison invests heavily in anti-aging research.

- Biohacker Bryan Johnson follows a strict daily routine designed to reverse his biological age.

These aren’t just casual health goals. These individuals are investing millions into personalized regimens, strict diets, advanced medical treatments, and experimental science all in pursuit of extending life.

Some even believe that if they can just make it to around 120 years old, future science might allow them to live indefinitely.

Yeah… basically, “live long enough to live forever.”

The Twist: Getting Paid to Live Longer

Here’s where things get really interesting.

There’s a concept in finance called longevity insurance and it flips traditional insurance on its head.

Normally, life insurance pays out when you die. But longevity-based financial products reward you for doing the opposite: staying alive longer than expected.

According to financial experts, longevity insurance works like a “reverse life insurance.” Instead of paying your family after death, it provides income if you live far beyond average life expectancy.

Think of it like this:

- You invest early.

- You survive longer than most people.

- You start receiving payouts later in life (like at 85, 90… or beyond).

In simple terms: you win by not dying.

Why This Exists: The Longevity Risk Problem

This might sound cool, but it actually comes from a real financial problem: longevity risk.

Longevity risk is the danger that people live longer than expected and run out of money. Governments, pension systems, and insurance companies are all struggling with this.

Because if people start living to 100… or 120… retirement systems break.

That’s why new financial products are emerging to handle this reality. And for the wealthy, these tools aren’t just protection, they’re strategy.

Billionaires Treat Longevity Like an Investment Portfolio

Here’s the mindset shift: billionaires don’t see health as just “wellness.”

They see it as ROI (return on investment).

Instead of spending money to treat illness, they spend aggressively to prevent aging itself.

Typical strategies include:

- Personalized medical teams

- Advanced diagnostics and full-body scans

- Stem cell therapies and experimental drugs

- Strict nutrition and fitness protocols

- Continuous health tracking

These aren’t casual habits. They’re optimized systems designed to extend both lifespan and “healthspan” (how long you stay healthy).

Some even follow extreme routines fasting for hours daily, tracking every calorie, and optimizing sleep like it’s a business metric.

The Business of Living Longer

The crazy part? This isn’t just personal, it’s a massive industry.

The anti-aging and longevity market is expected to reach hundreds of billions of dollars globally.

Why?

Because aging is the ultimate universal problem.

Everyone wants more time but only a few can currently afford the most advanced solutions.

This creates a huge gap:

- The wealthy invest in cutting-edge life extension.

- The average person gets traditional healthcare.

And that gap could widen dramatically if breakthroughs actually work.

The Dark Side: Is This Just a Rich People Game?

Not everyone is hyped about this.

Critics argue that the obsession with living longer is less about improving life and more about avoiding death at all costs.

Some believe it’s driven by fear rather than purpose.

And there’s a real ethical question:

What happens if only the rich can afford to live significantly longer?

Imagine a world where billionaires routinely live to 120 while everyone else doesn’t.

That’s not just a health issue, it’s a societal shift.

The Reality Check: Can Humans Actually Reach 120?

Right now, the longest confirmed human lifespan is 122 years.

So technically, it’s possible but extremely rare.

Science is making progress, but there’s still no guaranteed way to consistently reach 120, let alone go beyond it.

Many experts say we can extend healthy years but “immortality” is still far away.

Even among billionaires, results are uncertain.

The Future: A World Where Living Longer Pays

Despite the uncertainty, one thing is clear:

Longevity is becoming financialized.

In the future, we might see:

- More “live longer, earn more” insurance products

- Investments tied to health outcomes

- Personalized longevity plans like retirement portfolios

- Entire economies built around extending human life

For billionaires, this is already happening.

They’re not just trying to live longer they’re betting on it.

Final Thoughts: The Ultimate Flex?

So yeah… getting paid to stay alive sounds wild but it’s real.

For the ultra-wealthy, longevity is no longer just about health. It’s a mix of science, finance, and ambition.

They’re essentially asking:

What if death… was optional (or at least delayed)?

And more importantly:

What if surviving longer made you richer?

For now, it’s a game only a few can play.

But if science keeps evolving, this “billionaire bet” might one day become everyone’s reality.

Until then… staying alive is still free but maybe not for long.

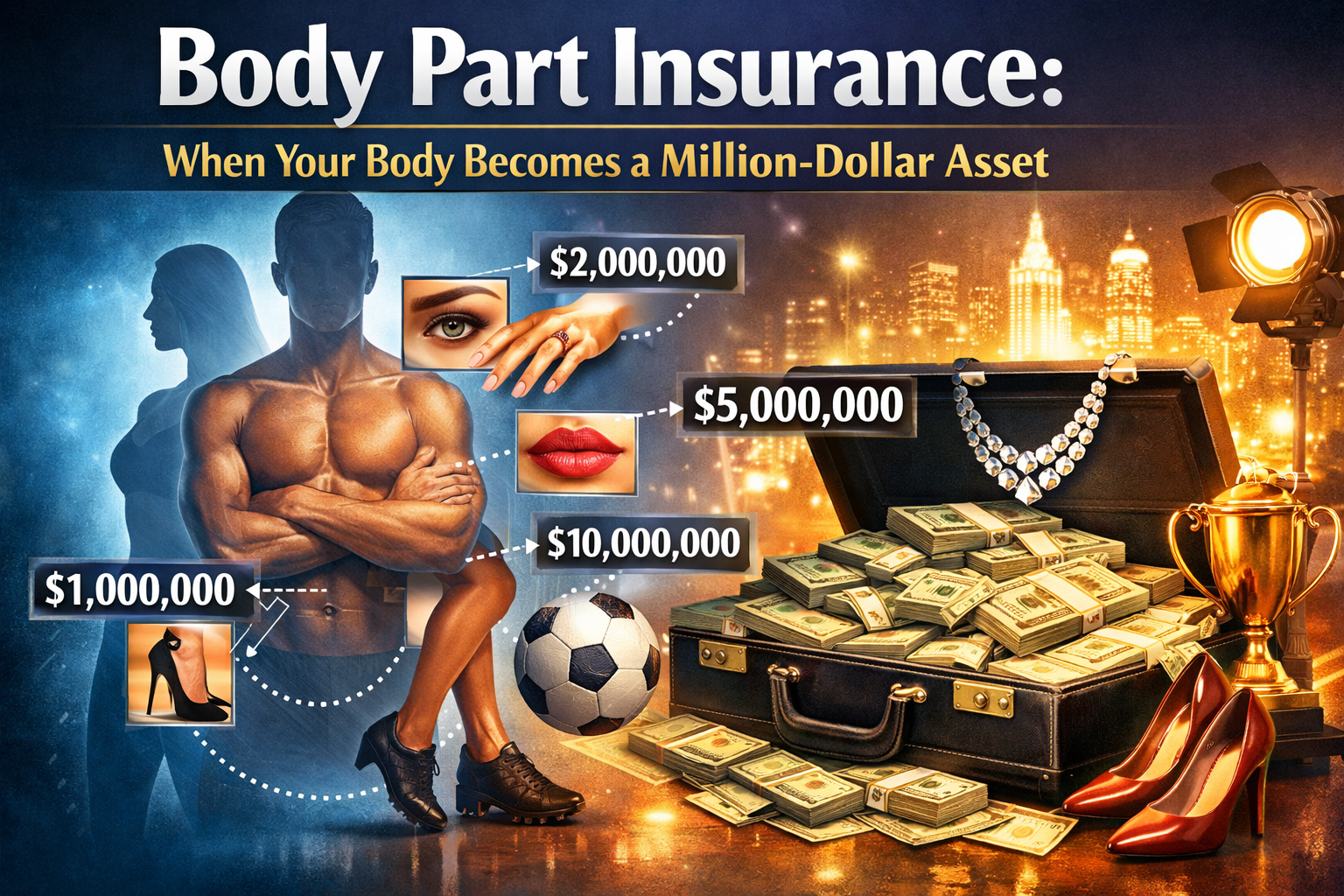

What if your lips were worth millions… or your hair… or even your taste buds? Sounds unreal, but in today’s world of celebrity branding and high-stakes careers, body part insurance is very real and getting bigger.

From Hollywood icons to athletes and even niche professionals, people are turning their physical features into protected financial assets. And the numbers? Absolutely insane.

What Is Body Part Insurance (Deeper Look)?

Body part insurance isn’t a standard policy you can just click and buy online. It usually falls under specialty insurance (often through companies like Lloyd’s of London).

Here’s how it works:

- A person identifies a body part critical to their income

- Insurers assess its value (based on earnings, brand deals, future potential)

- A policy is created to cover damage, loss, or reduced function

- If something happens → payout kicks in

It’s basically treating your body like a business asset.

How Do They Decide the Value?

This part is actually super interesting.

Insurance companies don’t just guess a number they calculate:

- Current income tied to that body part

- Future earning potential

- Market demand (how unique or recognizable it is)

- Risk level (injury chances, lifestyle, profession)

That’s how we end up with numbers like $300 million for legs 😳

More Crazy Real-Life Stories (Gets Wilder 👇)

⚽ David Beckham – The $195 Million Whole Body

David Beckham reportedly insured his entire body for around $195 MILLION.

Why? Because he wasn’t just a footballer he was a global brand. His looks, physique, and presence brought in massive endorsement deals.

🎸 Keith Richards – The $1.6 Million Hands

The legendary guitarist insured his hands for about $1.6 MILLION.

Without them? No guitar. No performances. No income. Simple.

🦵 Heidi Klum – Uneven Legs Worth Millions

Heidi Klum insured her legs—but here’s the twist:

- One leg was valued higher than the other 😭

Total value? Around $2 MILLION

Yes, even tiny differences matter at that level.

🍗 Betty Grable – The Original Million-Dollar Legs

Back in the 1940s, Betty Grable insured her legs for $1 MILLION—which today would be worth over $20+ MILLION adjusted for inflation.

She basically started the trend.

👃 Troy Polamalu – The $1 Million Hair

This one’s iconic.

Troy Polamalu insured his hair for $1 MILLION because it was part of his identity—and even featured in commercials.

👅 Rihanna – The $1 Million Legs

Rihanna reportedly insured her legs for $1 MILLION after winning a “best legs” award.

Brand deals + beauty recognition = $$$

The Weirdest Body Parts Ever Insured 🤯

This is where it gets kinda crazy:

- Taste buds → insured by professional food tasters

- Noses → perfume experts rely on them

- Beards → some celebrities have insured facial hair

- Chest hair → yes, even that has been insured 💀

- Butts → rumored in entertainment industry

Basically, if it can make money… it can be insured.

Can Normal People Do This?

Short answer: yes—but with limits

You don’t need to be a celebrity, but you do need:

- Proof that your income depends on that body part

- A high enough earning level

- A legit reason for risk coverage

Examples:

- A surgeon insuring their hands

- A dancer insuring their feet

- A YouTuber/influencer insuring their appearance

It’s rare but not impossible.

The Hidden Risks (Not All Glamorous)

This isn’t just flexing money—there are downsides too:

1. Expensive Premiums

You might pay thousands (or millions) yearly just to keep the policy active.

2. Strict Conditions

Some policies limit activities:

- No extreme sports

- No risky behavior

- Lifestyle monitoring 👀

3. Claim Challenges

Insurance companies investigate claims deeply. You can’t just say “my voice is off today” and expect millions.

The Business Side of It

This whole industry is growing because of:

- Influencer economy

- Personal branding

- Social media fame

- High-value endorsements

Today, a face or voice can be worth more than a traditional job.

So people are thinking:

“If I insure my car… why not my face?”

Future of Body Part Insurance

This is where things get even more interesting.

In the future, we might see:

- Influencers insuring their Instagram face

- Gamers insuring their hands & reaction time

- AI creators insuring their voice clones

- Virtual influencers insuring digital identity

Yeah… it’s going to get even crazier.

Final Thoughts

Body part insurance might sound like a flex, but it’s actually:

👉 Smart risk management

👉 Brand protection

👉 Financial securityIn a world where you are the product, protecting your most valuable asset just makes sense.

Casinos com Multibanco em Portugal: tudo o que precisas saber

Get Paid to Stay Alive? The Billionaire Bet on Living to 120

Body Part Insurance: When Your Body Becomes a Million-Dollar Asset

How Much Is Health Insurance a Month?

Will Insurance Cover Ozempic? This Information Tells You the Truth

What Does Life Insurance Cover?7 Must-Known Facts to Protect Your Loved Ones!

-

Health Insurance1 year ago

How Much Is Health Insurance a Month?

-

General Insurance1 year ago

Will Insurance Cover Ozempic? This Information Tells You the Truth

-

Life Insurance1 year ago

Life Insurance1 year agoWhat Does Life Insurance Cover?7 Must-Known Facts to Protect Your Loved Ones!

-

Auto Insurance1 year ago

Auto Insurance1 year agoWhy Is My Auto Insurance So High? There Is a Secret Behind High Auto Insurance Costs That Goes Unknown

-

General Insurance4 months ago

Can Cowboys Get Life Insurance?

-

Life Insurance1 year ago

Life Insurance1 year agoWhat Is Life Insurance? Everything You Need to Know!

-

Health Insurance3 months ago

Health Insurance3 months agoMobility Scooter Insurance: What It Is, Why You Need It, and How to Choose the Best Policy

-

Health Insurance3 months ago

Health Insurance3 months agoPrima Car Insurance Reviews: Is It the Right Choice for Your Ride?